You applied for a loan. Or a credit card. And something came back lower than you expected.

A three-digit number quietly shaped that outcome — and most people have no clear idea how it works or what actually moves it.

Your credit score in India, most commonly your CIBIL score, affects more of your financial life than you might realize. Understanding what it is, what damages it, and how to improve credit score India is one of the most practical things any earning adult can do for their long-term financial health.

Why Credit Score Confusion Is So Common in India

Credit scoring as a mainstream financial concept is relatively recent in India. For most of the previous generation, borrowing happened through personal relationships, community trust, and informal networks. A formal credit score was either irrelevant or invisible to the average person.

That has changed dramatically. Today, almost every significant financial decision — a home loan, a car loan, a personal loan, a credit card application, sometimes even a rental agreement — involves a credit score check. The number has become genuinely important to everyday financial life.

But awareness of how credit scores work has not kept pace with how frequently they are being used.

Most people in India encounter their credit score for the first time when they apply for something and are either denied or offered worse terms than they expected. That is a difficult moment to begin understanding the concept — under pressure, after the fact, when the damage has already been done.

The result is a widespread gap between the importance of the credit score in modern Indian financial life and the average person’s understanding of what drives it, what hurts it, and what actually helps it recover.

What a Credit Score Actually Is and Why It Exists

A credit score is a numerical summary of your credit history — a reflection of how reliably you have borrowed and repaid money over time. In India, the most widely used score is the CIBIL score, maintained by TransUnion CIBIL. Scores range from 300 to 900. A score above 750 is generally considered good by most lenders.

The score exists because lenders need a standardized way to assess risk before extending credit. Rather than reviewing every loan application from scratch, they use your credit history — compiled into a score — as a starting signal. A higher score suggests a lower risk of default. A lower score suggests the opposite.

Your credit report, which the score is based on, contains your entire history of credit accounts — loans, credit cards, overdrafts — including how much you borrowed, how much you still owe, and whether you paid on time.

Understanding this foundation matters because it clarifies something important: your credit score is not a judgment of your worth or financial intelligence. It is a data summary of specific financial behaviors over a specific period of time. That means it can be understood, managed, and over time, genuinely improved.

What Actually Affects Your Credit Score in India

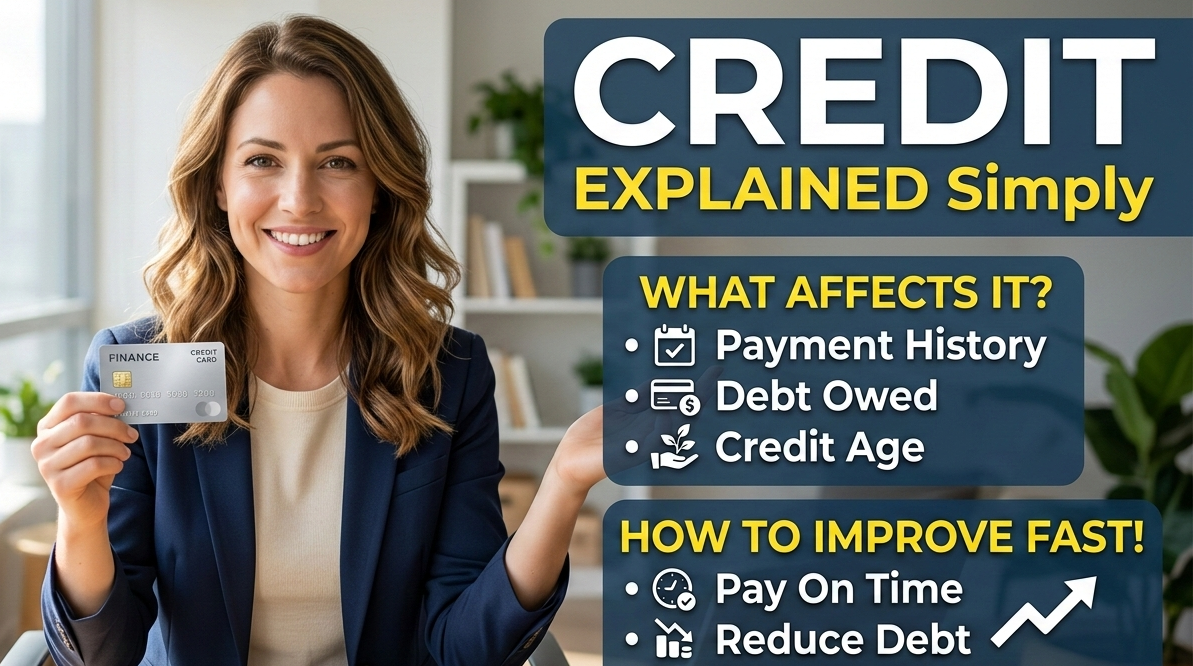

Before understanding how to improve credit score India, it helps to understand what the score is built from. There are five primary factors that influence it, though their exact weightings are not publicly disclosed by CIBIL.

Payment History — The Most Important Factor

Whether you pay your EMIs and credit card bills on time is the single most significant input into your credit score. A single missed payment, especially on a credit card or loan EMI, can cause a meaningful drop in your score. Multiple missed payments over time cause severe and lasting damage.

This is the factor that most directly reflects the behavior lenders care most about — will this person repay what they borrow, when they are supposed to repay it?

Credit Utilization Ratio

Your credit utilization ratio is the percentage of your available credit limit that you are currently using. If your credit card limit is ₹1,00,000 and your current outstanding balance is ₹60,000, your utilization ratio is 60 percent.

High utilization — generally above 30 to 35 percent — signals to lenders that you are heavily dependent on credit and may be financially stretched. It negatively affects your score even if you pay on time. Keeping utilization low is one of the most actionable CIBIL score tips available.

Length of Credit History

The longer your credit history, the more data is available for the scoring model to work with. A person with ten years of responsible credit use has a more reliable track record than someone with ten months, even if both have paid on time.

This is why closing old credit card accounts can sometimes hurt your score — it shortens your average credit history and reduces your total available credit limit, both of which can negatively affect the calculation.

Credit Mix

Having a healthy mix of credit types — secured loans like a home loan, unsecured loans like a personal loan, and revolving credit like a credit card — generally reflects positively on your score. It demonstrates that you can manage different forms of credit responsibly.

This does not mean taking on unnecessary debt to improve your mix. But it does explain why someone with only one type of credit account may have a harder time building a high score quickly.

Recent Credit Inquiries

Every time you apply for a new loan or credit card, the lender makes a hard inquiry on your credit report. Each hard inquiry causes a small, temporary dip in your score. Multiple hard inquiries in a short period — applying for several loans or credit cards within weeks of each other — signal financial desperation to lenders and can noticeably damage your score.

What Most People Misunderstand About Credit Scores

Checking Your Own Score Does Not Hurt It

This is one of the most persistent and damaging myths around credit scores in India. Many people avoid checking their own credit score because they believe the act of checking it will lower it.

This is incorrect. Checking your own score is a soft inquiry and has no impact on your score whatsoever. You can check your credit report as often as you want without any negative consequence. In fact, checking it regularly is one of the most useful habits you can build, because it allows you to catch errors, track progress, and identify problems early.

A Zero Credit History Is Not a Good Credit History

Some people take pride in never having borrowed money. No loans, no credit cards, no debt of any kind. From a personal values perspective, that is entirely valid. From a credit score perspective, it creates a problem.

With no credit history, lenders have no data on which to assess your reliability. You do not have a high score. You have no score, or a very low one, which is almost as limiting when applying for significant credit like a home loan.

Building a credit history responsibly — using a credit card for regular purchases and paying the full balance every month, for example — creates the track record that a good credit score requires.

Closing a Credit Card Does Not Always Help

Many people close unused credit cards thinking it will clean up their financial profile or improve their score. In practice, closing a credit card can hurt your score in two ways.

First, it reduces your total available credit limit, which can push your utilization ratio higher even if your spending stays the same. Second, if it is an old account, closing it shortens your average credit history. Unless there is a compelling reason — high annual fees, a specific financial restructuring plan — keeping old credit cards open and occasionally used is often better for your score than closing them.

One Late Payment Can Have Outsized Impact

People sometimes assume that a single missed payment among years of on-time payments will barely register. In reality, payment history carries significant weight, and a single missed or delayed payment — especially on a credit card — can drop a good score by a meaningful amount.

The score is not an average. It is sensitive to recent negative events. A long history of good payments helps over time, but it does not make a recent missed payment invisible.

A Real-Life Example Worth Considering

Consider a young professional in Mumbai who had never owned a credit card and had no loans. When she applied for a home loan at 28, she was surprised to find her CIBIL score was low — not because of any negative history, but because she had no credit history at all. She had been financially responsible her entire adult life, but the scoring system had no evidence of that.

She spent the next eighteen months building her credit profile carefully — a secured credit card used for small regular purchases, always paid in full, and a small personal loan repaid on time. By the time she reapplied, her score had crossed 750 and she received significantly better loan terms.

Her experience was not about fixing damage. It was about building a history that had never existed.

How to Improve Credit Score India — What Actually Works

This is not a list of shortcuts. Genuine credit score improvement in India takes time and consistent behavior. But the behaviors that move the score are well understood.

Pay Every Due Date Without Exception

This is the single most impactful action available. Set up automatic payments for at least the minimum amount due on every credit account, so that even in a busy or difficult month, you never accidentally miss a payment. Pay the full outstanding balance whenever possible to avoid interest accumulation.

Keep Credit Utilization Below 30 Percent

If your total credit card limit is ₹1,50,000, try to keep your monthly outstanding balance below ₹45,000 to ₹50,000. If you regularly use more than 30 percent of your limit, consider requesting a limit increase — which reduces your utilization ratio without requiring you to spend less — or spreading spending across cards if you have more than one.

Do Not Apply for Multiple Credit Products at Once

Each application triggers a hard inquiry. If you are planning to apply for a significant loan, avoid applying for any other credit in the months leading up to it. Space out credit applications and apply only when you have a genuine need.

Review Your Credit Report Regularly for Errors

Errors in credit reports are more common than most people realize. A loan that was fully repaid but still shows as outstanding. An account that does not belong to you. A payment marked late when it was made on time. These errors directly damage your score without any fault on your part.

Checking your credit report regularly and raising disputes for any inaccurate information is one of the most straightforward CIBIL score tips available — and one of the most consistently overlooked.

Build History Gradually and Patiently

If you are starting from a low score or no score, the path forward is gradual. A secured credit card, used responsibly. A small loan repaid on time. Consistent payment behavior over twelve to twenty-four months. The score responds to sustained good behavior, not to any single action.

There is no legitimate shortcut to a high credit score. Anyone suggesting otherwise is either mistaken or misleading.

The Subheading That Matters: Improve Credit Score India Through Consistency, Not Cleverness

The most important thing to understand about improving your credit score in India is that the score rewards the same behaviors that good financial management rewards — paying on time, not overextending credit, maintaining a long and stable credit history, and not desperately chasing new credit.

There is no clever trick that bypasses consistent responsible behavior. The score is a reflection of a pattern over time. Changing the score means changing the pattern — and that takes time.

People who improve their CIBIL score meaningfully over twelve to twenty-four months do so by doing the same few things correctly and repeatedly. Not by gaming the system. Not by following complex strategies. By paying on time, keeping utilization low, and letting the history build.

Clear Takeaway: Your Credit Score Is a Reflection of Habits, Not a Fixed Verdict

Your credit score is not permanent. It is not a life sentence. It is a current snapshot of a financial history that you are actively writing every month.

A low score today reflects past behavior, some of which may have been unavoidable. A high score in the future reflects the habits you build from this point forward. The two are connected by time and consistency — there is no other path between them.

To improve credit score India, start with full visibility. Get your credit report. Understand what is in it. Identify the specific behaviors that are hurting your score. Then address them one by one, patiently and consistently.

The score will follow.

A Final Thought on Trust and the Long Game

Building a strong credit score is, at its core, about building a financial reputation over time. It is a record of how reliably you honor your financial commitments — to lenders, to institutions, and in a quiet way, to yourself.

That reputation is not built quickly. It is not built through any single brilliant decision. It is built through hundreds of ordinary decisions made correctly over months and years. Pay this bill on time. Keep this balance low. Do not take on credit you do not need. Check this report and fix this error.

None of these actions is dramatic. Together, sustained over time, they produce a credit profile that opens financial doors — better loan terms, lower interest rates, easier approvals — that genuinely matter to the quality of your financial life.

The three-digit number is just the summary. The real work is in the habits behind it. FOLLOW FOR MORE..