It started with one easy EMI.

Then another. Then one more because the offer was too good to ignore.

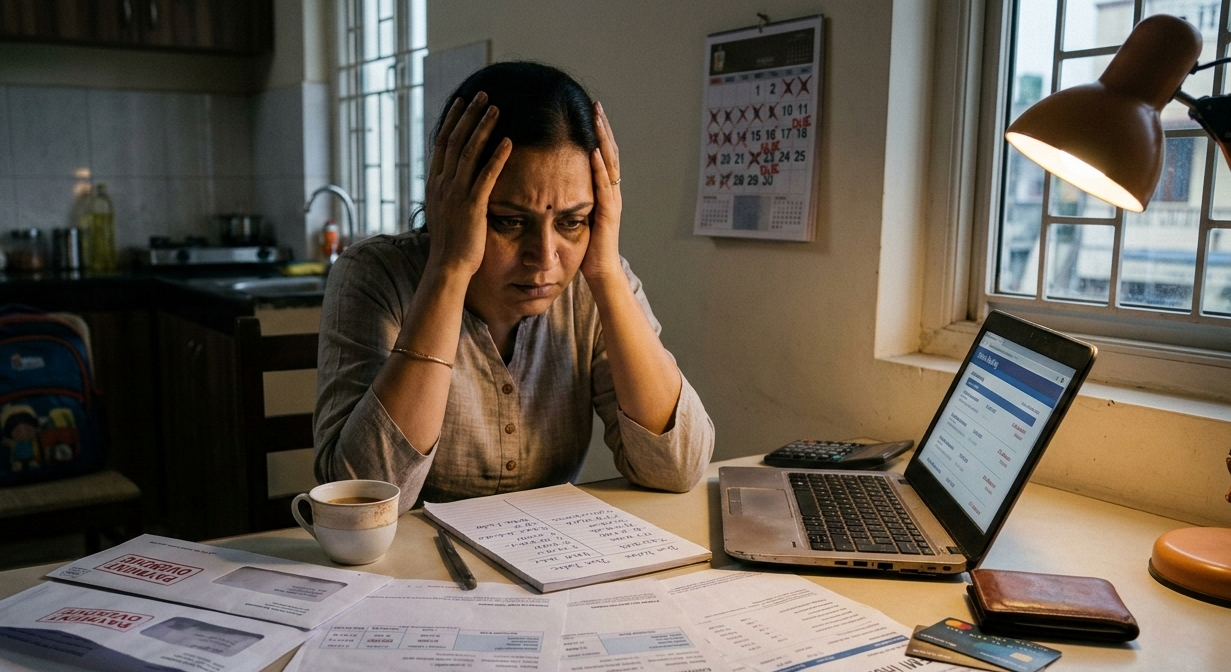

Now a significant chunk of your salary is gone before you even decide where it goes — and the weight of it sits somewhere between your chest and your monthly bank statement.

Why EMI Problems Have Become So Normal in India

A decade ago, taking a loan was a considered decision. It involved paperwork, a branch visit, a waiting period, and a conversation with a bank manager. That friction, while inconvenient, also created a natural pause. People had time to think before committing.

That friction is almost entirely gone now.

Today, EMI problems begin with a single tap. Buy now, pay later. Zero down payment. No-cost EMI. Instant approval. Pre-approved loan offers waiting in your inbox. The entire lending ecosystem has been redesigned around removing hesitation and accelerating the decision to borrow.

This is not an accident. It is a business model.

Every convenience layered onto the borrowing process is designed to reduce the psychological weight of taking on debt. And it works. People who would have paused before a formal loan application will tap through a three-step EMI checkout without a second thought. The commitment feels small because the monthly number looks small.

But small monthly numbers across multiple commitments add up into a loan stress that is very large indeed.

The structural shift in how credit is offered has outpaced most people’s awareness of how credit actually works. EMI problems in India today are not primarily the result of financial irresponsibility. They are the predictable outcome of a credit environment that has made borrowing effortless without making its consequences equally visible.

The Real Reason EMI Burden Grows Without Warning

Most people who are under EMI stress did not take one large reckless loan. They took several reasonable-sounding ones over time.

A home loan — entirely justified, a long-term asset. A car loan — necessary for work. A personal loan during a family emergency. A consumer durable loan for a phone or appliance that seemed practical. A credit card EMI conversion for something that felt urgent at the time. Each decision, viewed individually, had a reasonable justification.

This is how EMI problems actually develop. Not through one dramatic mistake, but through a slow accumulation of individually defensible commitments that were never evaluated together.

The human brain is good at assessing single decisions. It is significantly less good at tracking the cumulative weight of many simultaneous commitments. Each new EMI is evaluated against your income at that moment, not against the total obligation you are already carrying. By the time the full picture becomes visible, the salary is already heavily committed.

There is also a timing effect. Loans feel manageable at the point of taking them because your future feels optimistic. You expect income to grow. You assume expenses will stay roughly the same. You do not fully account for the possibility of job changes, medical expenses, family obligations, or the simple reality that life rarely stays predictable for the full tenure of a five-year loan.

Loan stress does not announce itself at the beginning. It builds quietly, installment by installment, until one month something shifts and the numbers no longer work the way they used to.

What Most People Misunderstand About EMI and Debt

The Monthly Amount Is Not the True Cost

When most people evaluate an EMI, they look at one number: the monthly installment. Can I manage this amount every month? If the answer is yes, the loan feels affordable.

This is the most common and most costly misunderstanding around EMI problems.

The monthly installment is not the true cost of a loan. The true cost is the total amount repaid over the entire tenure, including all interest. A loan that feels affordable at ₹4,000 per month for five years actually costs you ₹2,40,000 — and depending on the interest rate, the actual purchase may have cost you significantly more than its original price.

Most people never calculate this number. The lending process does not make it prominent. The monthly amount is featured. The total repayment is buried.

Zero-Cost EMI Is Rarely Zero Cost

The phrase “no-cost EMI” has become ubiquitous in Indian retail and e-commerce. It sounds like borrowed money with no penalty. That framing is almost always misleading.

No-cost EMI schemes typically involve costs that are structured differently — processing fees, the removal of a cash discount that would otherwise apply, or interest costs absorbed into the product price. The cost exists. It is simply presented in a way that makes it invisible to the buyer in the moment of purchase.

This is not illegal. But it is a significant source of EMI problems for people who genuinely believe they are borrowing for free and therefore borrow more freely than they otherwise would.

Your EMI-to-Income Ratio Matters More Than Any Single EMI

Financial planning guidelines generally suggest that total monthly EMI commitments should not exceed 40 to 50 percent of take-home salary. Beyond that threshold, the risk of loan stress rises sharply because there is insufficient buffer for unexpected expenses, savings, or any disruption to income.

Most people do not know their EMI-to-income ratio. They know their individual EMI amounts but have never added them together and divided by their salary. When they do this calculation for the first time, many discover they are already beyond a healthy threshold — sometimes significantly so.

Prepayment Feels Painful But Often Is Not

Many people avoid prepaying loans because losing a lump sum feels worse than paying a smaller amount every month. This is present bias at work again — the immediate pain of parting with a large amount outweighs the abstract future benefit of reduced interest and a shorter loan tenure.

In practice, prepaying even a portion of a high-interest loan can meaningfully reduce total repayment cost. The math almost always favors prepayment. The psychology resists it. Understanding this gap is part of developing a realistic relationship with debt management.

A Real-Life Example Worth Reflecting On

Consider a software professional in his early thirties in Hyderabad. Stable income, no obvious financial recklessness. Over four years, he had taken a home loan, a car loan, converted two large credit card purchases into EMIs, and taken a small personal loan during a family medical situation.

Each decision had felt manageable at the time. Together, his total monthly EMI commitment had reached 68 percent of his take-home salary. He was not defaulting. But he had almost no liquidity, no savings buffer, and a level of monthly financial pressure that had begun affecting his sleep and his professional focus.

His problem was not any single loan. It was the invisible accumulation of several reasonable ones over time. That is the quiet nature of the EMI trap — it rarely looks like a trap when you are stepping into it.

How EMI Problems Actually Develop Into Long-Term Loan Stress

Understanding the stages helps make the pattern visible before it becomes unmanageable.

Stage One — The Comfort Zone

Early EMIs feel fine. The salary covers them comfortably. There is money left over. The monthly installment feels like a small price for something valuable. This stage creates a false sense of how much debt capacity actually exists.

Stage Two — The Addition Problem

A second or third EMI is added. Each one still feels individually manageable. The total has grown but the full picture has not been evaluated. Savings begin to reduce slightly. Discretionary spending adjusts unconsciously to compensate.

Stage Three — The Squeeze

A new expense arrives — medical, family, home repair — and there is very little liquidity to absorb it. A credit card is used, which later gets converted into another EMI. The salary is now heavily committed. Any disruption to income creates immediate stress. This is the stage where loan stress becomes a daily experience rather than an occasional worry.

Stage Four — The Trap

At this stage, new borrowing is being used to manage existing borrowing. A personal loan to cover a credit card balance. An overdraft to bridge a salary gap. Each solution creates a new EMI, deepening the cycle. Getting out requires a structured approach, patience, and often a significant lifestyle adjustment.

Most people enter the trap gradually and do not recognize which stage they are at until stage three or four.

What Actually Helps With EMI Problems and Debt Management

This section is not about quick fixes or financial shortcuts. It is about what genuine debt management looks like in practice.

Calculate Your True EMI-to-Income Ratio First

Before anything else, add up every monthly EMI commitment you currently carry — home loan, car loan, personal loans, credit card EMIs, buy-now-pay-later installments, everything. Divide that total by your take-home monthly salary. Multiply by 100.

That number is your EMI-to-income ratio. Seeing it clearly, for the first time, changes how you relate to future borrowing decisions. It is the most important number most people never calculate.

Understand the Difference Between Asset-Building and Consumption Debt

Not all debt is equal in its long-term impact. A home loan builds an asset over time. A personal loan for a vacation or a consumer durable depreciates immediately. Understanding which category each loan falls into does not make consumption debt wrong, but it does make the true cost more visible.

Debt management becomes clearer when you can distinguish between debt that is building something and debt that has already been consumed.

Stop Adding Before You Start Reducing

One of the most effective early steps in managing EMI problems is simply stopping new EMI commitments while existing ones are still heavy. This sounds obvious. It is harder in practice because the offers keep coming and each one is framed attractively.

A personal rule that no new EMI will be added until the current EMI-to-income ratio drops below a specific threshold is a concrete and effective boundary. It does not require perfect willpower. It just requires a clear line that you have decided in advance.

Prioritise High-Interest Debt First

Not all loans cost the same. Credit card debt and personal loans typically carry significantly higher interest rates than home loans. When resources allow for any additional repayment, directing them toward the highest-interest debt first reduces total repayment cost most efficiently.

This is the principle behind what debt counselors call the avalanche method — not because it is dramatic, but because it is mathematically sound.

Build a Small Liquidity Buffer Before Aggressive Repayment

One of the reasons people fall deeper into debt is the absence of any financial buffer. Every unexpected expense goes onto a credit card or becomes a new loan because there is nothing else to absorb it.

Building even a modest emergency fund — enough to cover one or two months of essential expenses — before aggressively paying down debt creates a protective layer. It breaks the cycle where every new expense becomes new debt.

The Subheading That Matters: EMI Problems Are a Pattern, Not a Personality

One of the most important things to understand about EMI stress and loan burden is that it does not reflect character. It reflects a pattern — a series of individually reasonable decisions made without visibility into the full picture.

People who are under significant EMI stress are not careless. They are often the opposite — people who said yes to things that seemed responsible at the time. A home for the family. A reliable vehicle. A phone needed for work. The judgment was reasonable. The pattern, unmonitored, became a burden.

Recognizing this is not about removing accountability. It is about approaching debt management from a position of calm clarity rather than guilt and shame. Guilt does not pay down loans. Clear thinking and consistent action do.

Clear Takeaway: Visibility First, Then a Plan

EMI problems rarely announce themselves dramatically. They build gradually, across months and years, through a series of decisions that each felt small and sensible. By the time loan stress becomes impossible to ignore, the pattern has usually been forming for a long time.

The first step is not an aggressive repayment plan. It is an honest and complete picture of where you currently stand. Total EMI commitment. EMI-to-income ratio. Interest rates on each loan. Remaining tenures. Total amount still to be repaid.

That picture, seen clearly and without judgment, is the foundation of every debt management decision that follows. Without it, you are making decisions in the dark. With it, even a difficult situation becomes something you can work with systematically.

You are not trapped because you were foolish. You are in a tight spot because the system made it very easy to get there. That is a meaningful difference — and it is the right place to start.

A Final Thought on Time, Patience, and Getting Out Slowly

Getting into significant EMI burden typically takes years. Getting out also takes years. There is no shortcut that changes that fundamental reality, and any approach that promises otherwise is worth being skeptical of.

What debt management actually looks like, lived from the inside, is unglamorous. It is months of saying no to new commitments. It is redirecting small surpluses toward existing loans. It is rebuilding a savings buffer while simultaneously managing repayments. It is slow, and it requires patience with yourself when progress feels invisible.

But the direction matters more than the speed. Every month where no new debt is added is a month of genuine progress. Every small additional payment toward a high-interest loan is real. Every rupee moved into an emergency fund reduces the likelihood of the next unexpected expense becoming new debt.

EMI problems are solved the same way they were created — gradually, one month at a time. The difference is that this time, you are watching. FOLLOW FOR MORE...